YETI Holdings Shows Resiliency

Most supply chain issues have waivered.

Synopsis

Q3 2022 earnings showed 20% yoy growth

With costs normalizing, pressure on margins will ease

Continued focus on new markets, products, and sales channels

Background

Currently trading around $45 per share, YETI Holdings is down over 25% since last year. This sell off priced in many of the challenges YETI faced towards the end of last year. I believe many of these challenges have resolved themself, presenting some upside opportuntity.

Strong products and brand loyalty

Product quality is never questions. Reviews on products are 4+ stars. YETI continues to expand on its initial drinkware/coolers focus into outdoor living, travel, and lifestyle products.

Q3 report shows improvements in Direct to Consumer sales channels.

DTC channel sales increased 17% to $608.2 million, compared to $520.8 million in the prior year period, driven by Drinkware.

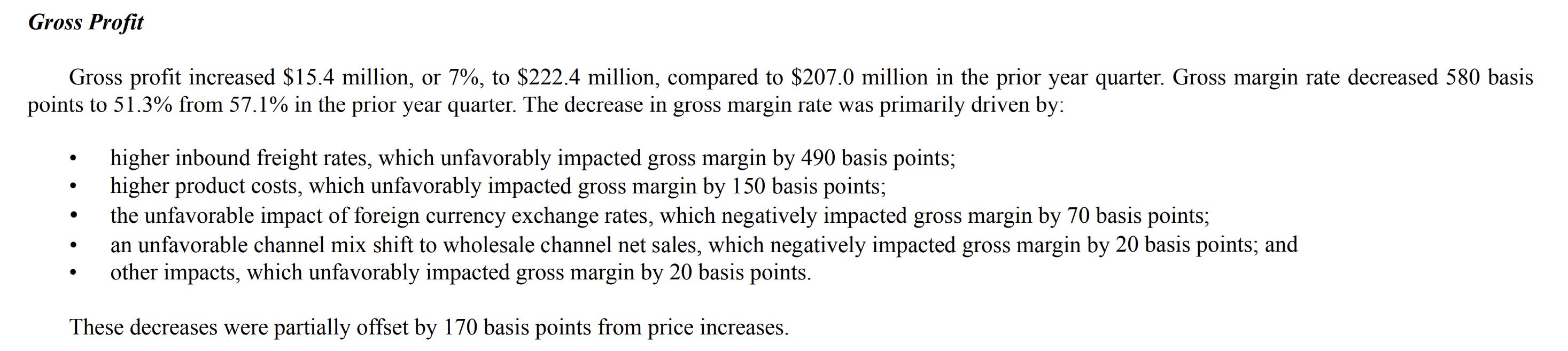

Freight Headwinds Over

Margins squeezed due to shipping container and domestic truckload rates. Both reversed and began easing in Q4 2022. These cost easing should be reflected in Q4 2022 earnings.

Conclusion

I believe the recent sell is an over exaggeration of supply chain issues and weak consumer confidence. I expect a 15-20% increase in share price prior to Q4 2022 earnings.

Concise actionable stock insights. Delivered to your inbox 2x week, enjoy snapshots of non-main streets stocks worth researching.

Join others and subscribe below. 👇

Nice, I plan on adding to my watchlist this week.